CLA is not an econometric-type model, nor is it based on any assumptions (i.e. guesses) as to future factors such as interest rates, employment statistics, GDP growth, or otherwise.

Instead, CLA applies mathematical and statistical techniques that are common practice in the insurance industry to objectively quantify risk and to forecast losses in a consumer loan portfolio. The analysis is based solely on the hard data mined from the client’s core IT system.

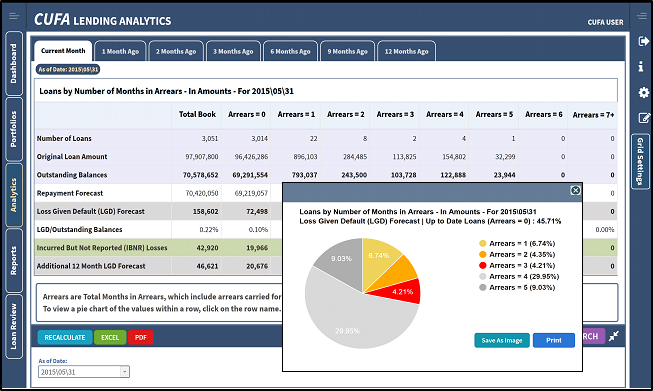

Unlike the other systems used for consumer loan risk analysis and provisioning, CLA computes the expected losses for loans that are not delinquent, along with incurred-but-not-reported (IBNR) losses that, in fact, have already impaired the actual value of the portfolio.

Virtually every ‘bad loan’ starts out as a ‘good loan’ that is not in arrears during the first month or so of its existence, and perhaps for many months more. The question CLA answers is how much loss can be anticipated from loans that are not (yet) in arrears, as well as from those that are.

Virtually every ‘bad loan’ starts out as a ‘good loan’ that is not in arrears during the first month or so of its existence, and perhaps for many months more. The question CLA answers is how much loss can be anticipated from loans that are not (yet) in arrears, as well as from those that are.

CLA therefore responds to a practical reality that is inherent in prudent consumer lending: Assuming good underwriting, consumer loans typically go bad for reasons that were basically unforeseeable when the loan was made and that are unlikely to reach the lender’s attention until after the loan falls into arrears. Those include the borrower’s job loss, ill health or substance abuse problems, marital difficulties, and so on.

There is, of course, no practical way of knowing whether any particular good loan will become a bad loan for such reasons. However, by employing the ‘law of large numbers’ CLA performs an analysis of each lender’s experience to forecast the percentages of loan types that will go bad for whatever reason (and when that will happen), at the portfolio, sub-portfolio and micro-portfolio levels.

The forecast is derived from the actual credit performance of the particular community of borrowers served by the lender. Because the data is refreshed monthly, CLA quickly picks up new risk trends resulting from recent changes in the environment that will impact future delinquency and default experience.

Conceptually, CLA’s analysis is similar to the actuarial analysis that enables a life insurer to project how many 30-year-olds will die in a particular year, so that it can set its pricing and claims reserves accordingly, even for policies issued without a health examination. The insurer does so based on mortality tables that reflect the actual experience of the relevant population.